Agency Model and E-commerce: Growing Trends in Automotive Retailing

Agency Model and E-commerce: Growing Trends in Automotive Retailing

As with most industries, digitization and increasing automation have revolutionized the automotive industry, giving rise to four major disruptive technological trends: electrification, autonomous driving, shared mobility, and connectivity. These trends, combined with demand and supply challenges such as declining purchasing power, increasing inflation, rising fuel prices, and reliance on Chinese supply, are putting pressure on automotive players to reconsider their current business models.

Since the invention of the automobile, the sales model has remained mostly the same. In the early 1900s, multiple distribution models were attempted in the auto industry; however, by the 1950s, the dealership model had proven to be the most effective for distributing automobiles. In this model, the manufacturer builds the vehicles and then sells them to dealers, which act as retailers and service providers.

Traditional sales models, however, have undergone fundamental changes in recent years as e-commerce and industry leaders revolutionized the purchasing process. Currently, new automotive players, such as EV startups, have started to adjust their sales model to adapt to evolving buying behaviors. Since 2016, EV pioneers like Tesla have been combining their city showrooms with their online stores, providing their customers with a simple interface and a brand-new purchasing experience when compared to traditional sales models.

The agency sales model: transforming the automobile purchase journey

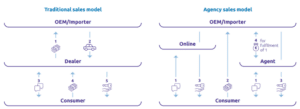

The agency sales model can be considered the evolution of the traditional three-tiered sales model towards an integrated online/offline sales model. In that sense, the vehicle manufacturers interact directly with the customers and assume all sales responsibilities. The dealers still play a decisive role in this model, but they act only as agents and only retain activities that require physical interaction, such as the execution of test drives and handling of service appointments.

The traditional sales model players, which include dealerships and national sales companies (NSCs), remain present in the agency model but are there to provide a superior omnichannel customer experience, allowing OEMs to establish a 360° customer view, resulting in increased cross-selling and market transparency.

Likewise, certain roles and responsibilities are transferred from the dealer to the manufacturer. The dealer’s financial risk can be reduced while gaining full access to the national car inventory and shortening delivery times.

Automotive retailing: a shift toward e-commerce

The online car buying market refers to the end-to-end purchase of vehicles through online platforms. This offers customers accessibility and ease of shopping from home, more visibility on pricing, and digital and secure payment processes.

Online vehicle sales have increased significantly in recent years. The global online car buying market was valued at $237.93 billion in 2020 and is projected to reach $722.79 billion by 2030. This market was not triggered by the pandemic in 2020, but rather is the result of the accelerated digitalization of car manufacturers and a shift in mindset and consumption behavior.

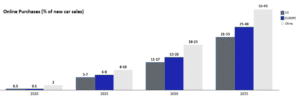

According to BCG projections, it is expected that online billing & payment transactions will account for 5-7% of new vehicle sales in 2025 and up to 33% in 2035. In terms of market share, Tesla continues to be the leader in direct sales, along with “Polestar”, which provides a mature online interface that challenges Tesla.

Online aftermarket sales: the rise of a new sales channel

The online automotive aftermarket is a secondary market accessed through e-commerce databases that sell almost all automotive spare parts, marketing services, and auto-related services.

Since the pandemic, the automotive aftermarket has registered an important evolution led by multiple trends, which can be perceived through the continuous global demand for used vehicles, auto parts becoming more sophisticated, and consumers holding onto their cars because of the financial downturn caused by the pandemic.

The whole automotive aftermarket sector (online & offline) is expected to grow from about $380 billion in 2021 to $449 billion in 2023. Moreover, the COVID-19 pandemic, along with the global disruption of the automotive supply chains, is acting as the main factors affecting buying behavior and leading a growing number of consumers toward the online aftermarket.

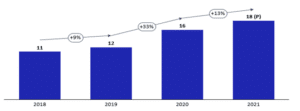

In that sense, according to Hedges & Company, online sales totaled $16 billion in 2020, a 40% increase from $7.4 billion in 2019 (figure 3). Similarly, business-to-consumer mobile sales also saw a significant increase in recent years, accounting for approximately 50% of all online auto part sales in 2020, an increase of 35% compared to the previous year.

Currently, the online aftermarket channels are being led by new players such as Car Parts and Mister Auto, whose business models are 100% online. Likewise, automotive manufacturers are also starting to respond to the current industry disruption by cooperating with online players to sell their parts and accessories.

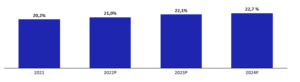

Growth of e-commerce automotive aftermarket

The trend of consumers looking for aftermarket products online has been accelerated by pandemic restrictions and the accelerated drive toward digitization in 2020 and 2021, which helped online sales channels increase their penetration rates (figure 4). The trend was most noticeable in the parts and accessories segment, which includes enthusiast and general maintenance DIY brands that experienced a sustained increase in sales in 2021.

Ultimately, a growing number of customers sought alternative channels for a variety of products, despite the fact that retailers were deemed essential service providers and operated during multiple shutdowns. As a result, retailers have been accelerating their digital solutions projects by improving e-commerce functionality and adding new shopping options, such as curbside pickup and faster home delivery.

The automotive industry is experiencing major changes in its landscape with digitization, electrification, and the complexity of the global market. Leading global players, including suppliers, OEMs, and new entrants, are already innovating their business models to adapt to the extremely competitive ecosystem. Even though the industry’s online penetration has increased in recent years, there are still plenty of opportunities for leaders to seize.

Success in 2030 will require automotive players to prepare for uncertainty, leverage partnerships (e.g., around infrastructure for autonomous and electrified vehicles), and reshape their value propositions. Concurrently, aftermarket players must improve their e-commerce strategies due to a greater emphasis on digital presence, as shoppers are becoming more accustomed to online channels due to the increased breadth, convenience, and ability to find exact specifications over traditional ones. Finally, as suppliers and retailers focus more intently on digital strategies to address consumer purchasing behavior, the e-commerce channel will continue to grow at an exponential rate in the automotive aftermarket.

Sources:

- https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/disruptive-trends-that-will-transform-the-auto-industry

- https://europe.autonews.com/guest-columnist/how-auto-industry-revolutionizing-its-sales-model

- https://home.kpmg/xx/en/home/insights/2022/08/changing-times-new-business-models-pose-challenges.html

- https://www.capgemini.com/wp-content/uploads/2021/09/Automotive-Agency-Sales-Model_POV_Capgemini-Invent.pdf

- https://www.alliedmarketresearch.com/online-car-buying-market-A10067

- https://www.jefferies.com/CMSFiles/Jefferies.com/Files/IBBlast/Industrials/IB-Autocare-2021-Review-and-Outlook.pdf

- https://f.hubspotusercontent20.net/hubfs/6890475/PDF-Premium-Downloads/Automotive-Aftermarket-2022-Report-Valtech-Absolunet-V2.pdf

- https://www.statista.com/statistics/1199431/online-car-sales-share-in-selected-markets-worldwide/

- https://www.simon-kucher.com/sites/default/files/2022-02/Brochure_Automotive-Study-2022.pdf

- https://www.precedenceresearch.com/aftermarket-automotive-parts-market

- https://www2.deloitte.com/content/dam/Deloitte/global/Documents/Consumer-Business/us-2022-global-automotive-consumer-study-global-focus-final.pdf

- https://www.globenewswire.com/en/news-release/2021/11/03/2326186/0/en/Global-E-Commerce-Automotive-Aftermarket-is-Anticipated-to-Reach-USD-132-75-billion-by-2028-Fior-Markets.html#:~:text=E%2Dcommerce%20automotive%20aftermarket%20provides,served%20by%20the%20market%20players.

- https://www.mckinsey.com/industries/automotive-and-assembly/our-insights/disruptive-trends-that-will-transform-the-auto-industry/de-DE