The Impact of COVID-19 in Latin America and the Caribbean

Table of Contents

The impact of COVID-19 in Latin America and the Caribbean has presented an unparalleled challenge for the global and regional economy. Nations are mobilizing every asset at their disposal to implement strategies aimed at alleviating the multifaceted crises—economic, financial, social, and health—induced by the pandemic, while concurrently exploring various methods to manage the virus’s proliferation and maximize life preservation.

While a lot of attention is, and must be, put in analyzing how governments are reacting today in order to learn how to better react in the face of a similar crisis sometime in the future, the crisis also demands a question: why are some countries responding better than others?.

The hard reality is that not all countries are facing the crisis from the same starting point. Developed countries are in a better position to face the different dimensions of the crisis due, to a large extent, to their available fiscal and healthcare resources. No country in the LAC region can afford the increases in public spending and investment carried out by developed countries in response to the pandemic, nor do they have the same access to international financing.

Developing regions such as Latin America and the Caribbean (LAC) must face large trade-offs when deciding where to allocate their available resources to respond to the effects of the crisis. Moreover, these tradeoffs are accentuated by the structural social inequality faced across the region. However, these limitations and conditions were not directly caused by the crisis that began at the start of the year, but rather the result of decades of policies that have created economies heavily burdened by social and economic vulnerabilities.

These vulnerabilities are a crucial factor when determining the region’s starting point in the face of the pandemic, the extent of the social and economic impacts, and its capacity to respond.

Projected impacts on the LAC economy and growth

As of January 2020, Latin America and the Caribbean (LAC) had projected GDP growth rates of 1.6% for 2020, and further 2.3% for 2021. However, these projections have drastically changed because of the crisis brought by the coronavirus pandemic. While the containment measures taken by LAC countries are bound to have an impact on their overall GDP growth, the uncertainty of how the pandemic will evolve, and how each country will respond, make estimations a very difficult exercise.

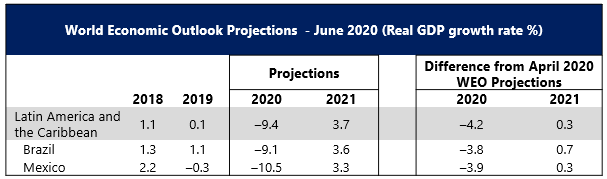

The projections from the June 2020 IMF World Economic Outlook indicate that Real GDP growth in Latin American and the Caribbean is estimated at -9.4% in 2020 but will return to a 3.7% growth in 2021. The 2 largest economies in the region, Brazil and Mexico will experience similar trend. These projections are vastly different from the estimations done earlier in April 2020.

These projections consider several key assumptions. For instance, the forecast factors a larger hit to activity due to the lockdowns in the first half of 2020, and a slower recovery in the 2nd half of the year compared to what was estimated during the April 2020 estimations. Productivity will be impacted as surviving businesses focus on improving workplace safety and hygiene standards. Countries struggling to control infection rates will need to extend the lockdown and social distancing measures. On the other hand, countries that have controlled infection rates will not reinstate stringent lockdowns and will rather rely on more targeted measures (i.e. contact tracing, isolation, etc.).

The projections also factor in the impact of the fiscal countermeasures implemented so far and anticipated of the rest of the year. The model also assumes that fuel prices are expected to remain broadly unchanged compared to the April 2020 version of the economic outlook, with average petroleum spot prices at $36.20 per barrel in 2020 and $37.50 in 2020, with expectations of an increase up to $46 (25% below the 2019 average). Nonfuel commodity prices are expected to rise faster than what was assumed in the April projections.

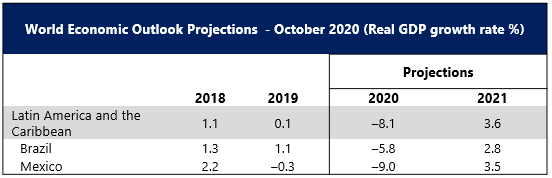

During October, the IMF released its update with new growth projections, showing that the economic impacts of the pandemic are hard to estimate. The new projections show more positive scenario for the region and its 2 largest economies in 2020, but with slightly lower growth estimates in 2021 for the region and Brazil.

We will likely see further changes in these projections as countries enter the year 2021, and actual figures for full-year 2020 become available.

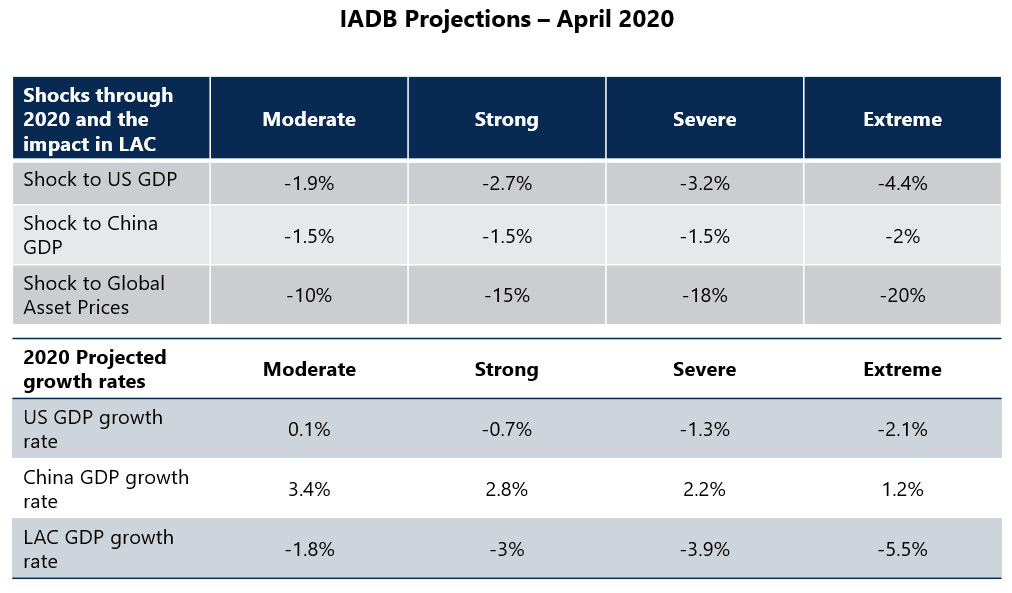

Earlier during April 2020, the Interamerican Development Bank (IDB) developed a model depicting 4 shock scenarios for the region, taking into account external factors such as: GDP losses in the US and China, with some recovery towards the end of 2020 and into 2021; asset price shocks and their impact in financial markets and capital flows; and commodity prices for oil, metal and agricultural products. The variables were chosen by the key assumption that the shock from the crisis is external, so no internal impact from the measures taken by the countries was considered for the model.

While the quantitative estimations might be outdated when compared to the IMF World Outlook projections, the different variables used for the model give some insight on how the crisis can impact countries and sub-regions differently. For example, low oil prices will have negative impact on major oil exporters such as Mexico, Colombia, Venezuela and Ecuador, while low metal prices will affect exporters such as Chile and Peru.

While metal and oil prices do not tend to affect employment or consumption, they do have a large impact in public revenues, output, and investment. On the other hand, the prices on agricultural products affect employment, consumption, and public revenues (i.e. export taxes).

Source: IADB

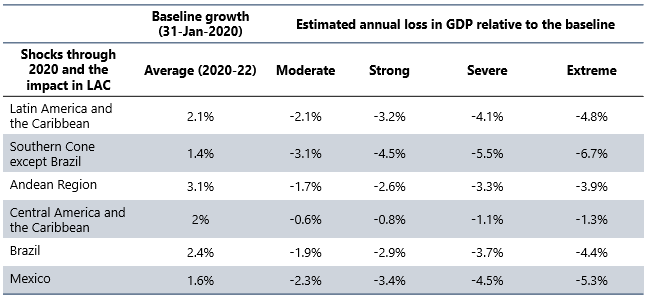

As per the IADB projections, the LAC region will lose between 6.3% and 14.4% of its’ GDP during the 2020-22 period.

The Southern Cone will be impacted mostly by commodity prices, but the dislocation of financial markets will also have a relevant impact, since countries in the sub-region tend to be financially integrated.

For the Andean region, the impact might seem low at sub-regional level, but specific cases might vary per country. Ecuador, as an oil exporter, will be impacted by the low prices and its financing needs, and it cannot use the exchange rate to absorb the shock because its economy is dollarized. A similar case might be observed for Colombia, which is an oil exporter that normally attracts foreign investments to finance current account deficits. Peru, on the other hand, will be impacted by copper prices, but has relatively low debt and good access to capital markets.

Mexico is also expected to suffer severe GDP losses, mainly because of its trade dependence with the US, globally integrated value chains and low oil prices.

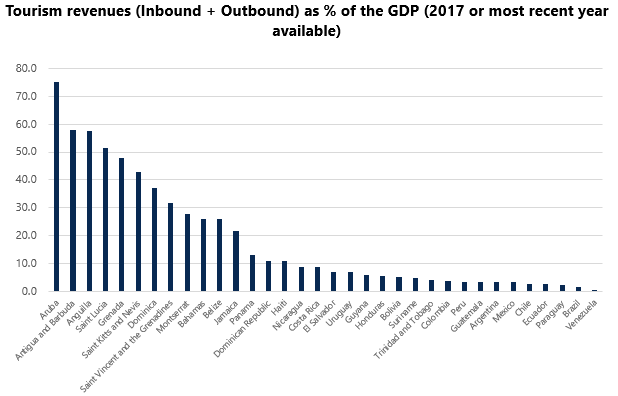

Central American and Caribbean countries can benefit from low oil prices, as they are mostly oil importers, but their GDP losses are mainly caused by the high dependence on the US for tourism revenues and remittances. In 2018, North America accounted for 69% of tourists in the Caribbean. Due to the current and expected travel restrictions, tourism in the Caribbean is expected to contract by 25%. Tourism represents 15.5% of the GDP in the Caribbean region, but the range of dependency varies greatly per country, as tourism expenditures represent 75% of Aruba’s GDP, compared to 4% for Trinidad & Tobago. The impact will also be felt directly in employment and household incomes, as the sector employs 2.4 million people in the Caribbean region.

Impact on Trade

Moreover, the pandemic will also have an impact on the already weak international trade prospects for the region, additional to decrease impact in commodity prices. The first phase of the US-China agreement in January, on which China pledged to increase its importance from the US by at least $77 billion in 2020, could potentially displace LAC as a trade partner for China in some product categories.

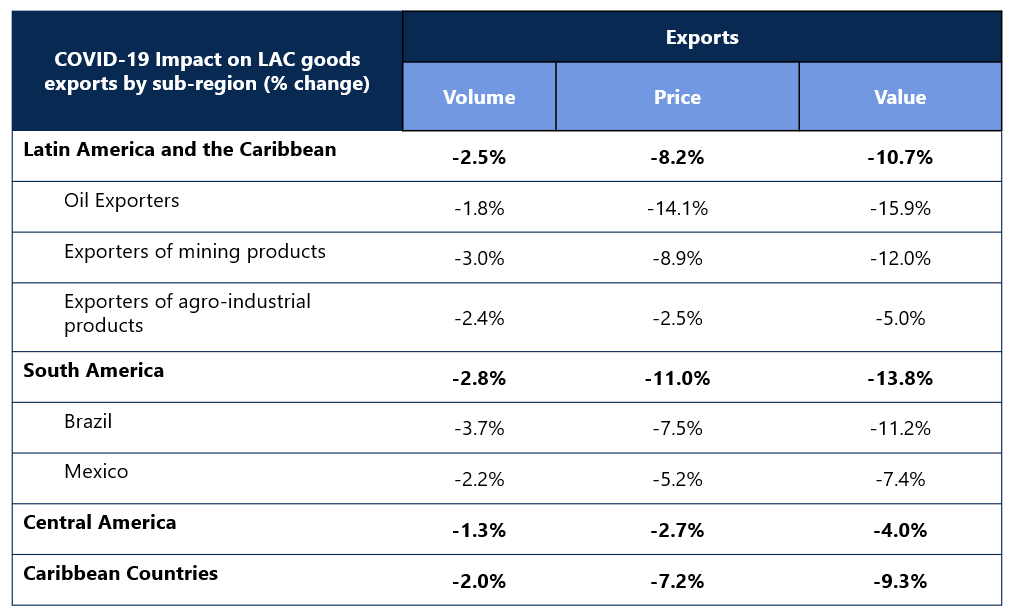

It is estimated that the value of LAC’s goods exports will be reduced by at least 10.7% by 2020, due to both a fall of 8.2% in prices and a 2.5% fall in export volumes.

Note: The following growth rates are assumed for 2020: 1.0% (world), 1.0% (United States), 0.3% (Japan), 0.5% (United Kingdom), -0.2% (European Union, 27 countries), 3.0% (China) and -1.8% (Latin America and the Caribbean), plus an average reduction of 16% in the region’s commodity export basket.

The greatest impact will be felt by the countries of South America, which specialize in the export of commodities, making them more vulnerable to a decrease in prices. In contrast, the value of exports from Central America, the Caribbean and Mexico would decrease less than the regional average due to their links with the US and their lower dependence on commodity exports. However, oil-exporting countries are expected to see the largest decrease in value.

The COVID-19 crisis may also have an impact on the region’s export performance because of its effect on imports used to produce exports. Some of the most affected countries will be Mexico and Chile, which receive 7% of their intermediate inputs from China, followed by Colombia and Peru, which import ~ 5% of their intermediate inputs from China.

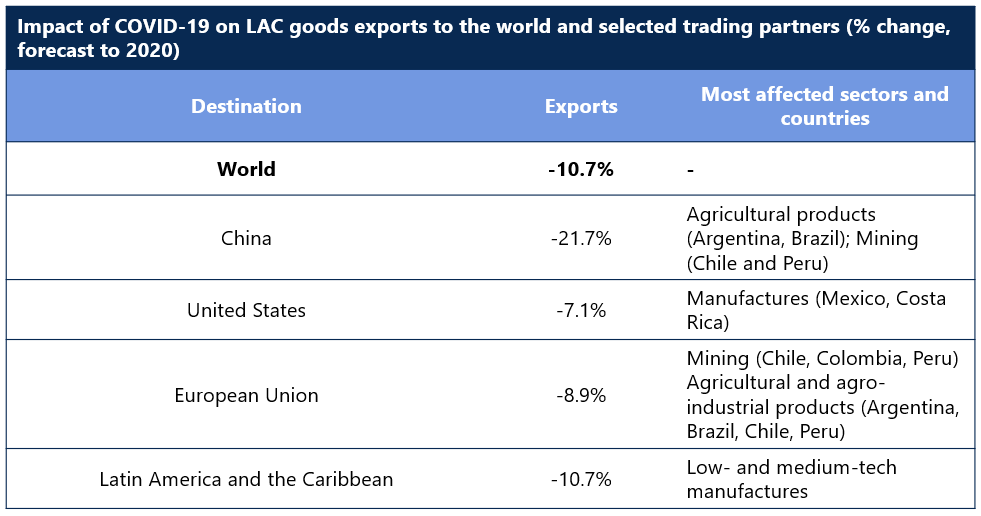

Regional exports to China are expected to fall the most in 2020 (-21.7%), affecting products with linkages in the value chains within China (iron ore, copper ore, zinc, aluminum, soybeans, soybean oil, etc.). The most exposed countries in the region are Argentina, Brazil, Chile and Peru, which are the region’s largest suppliers of such products to China.

Note: The following growth rates are assumed for 2020: 1.0% (world), 1.0% (United States), 0.3% (Japan), 0.5% (United Kingdom), -0.2% (European Union, 27 countries), 3.0% (China) and -1.8% (Latin America and the Caribbean), plus an average reduction of 16% in the region’s commodity export basket.

Regional exports to the US (-7.1%) and the European Union (-8.9%) are also expected to decrease to a lesser extent. Mexico is the country most exposed to changes in supply and demand conditions in the US, especially in the manufacturing sector. Costa Rica is also highly exposed to economic conditions in the US, as about 10% of its GDP depends on the United States supply and demand. The countries most exposed to changes in supply and demand conditions in the European Union are Chile, Mexico, and Brazil, as around 5% of their GDP depends on the service and manufacturing sectors.

Impact on Poverty and Employment

Given the region’s economic and social inequalities, the effects of the pandemic will disproportionally affect the poor vulnerable middle-income segments of the population. This will lead to an increase in informal employment and child labor, as the most vulnerable families will have to rely on these for survival.

Poverty in the region had already increased during 2014-2018, and the effects of the pandemic are very likely to increase the poverty and extreme poverty rates.

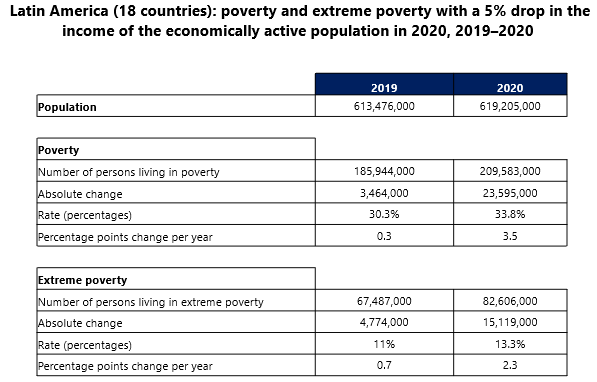

According to ECLAC estimations, if the effects of the pandemic lead to a 5% loss of income for the economically active population, the poverty rate can increase by 3.5 percentage points, while extreme poverty is expected to rise by 2.3 percentage points during 2019-2020, compared to an increase of 0.3 and 0.7 percentage points change respectively in the previous year.

People employed by micro, small or medium-sized enterprises (MSMEs) are a very vulnerable segment. Almost 99% of companies in the LAC region are MSMEs, and these represent the majority of companies in almost all economic sectors.

The temporary shutdown measures and restrictions on economic activities will lead to a significant decrease in sales revenues, putting the survival of these companies at risk. The economic impact numerous bankruptcies and closures MSMEs will have large social cost, given that these companies accounted for 61.1% of total employment in the region in 2016.

Regional Context

LAC governments face significant constraints in terms of their capacity to fight the effects of the pandemic. These constraints are not necessarily new, neither have they been caused by the pandemic. Rather, the pandemic has exhibited the many deficiencies in the institutional capacity of LAC countries due to decades of development policies that were not conductive to create sustainable and resilient economies.

The results of this are, to varying extents among countries, economies heavily burdened by dire fiscal spaces, and gaps in access to basic services.

Fiscal Space

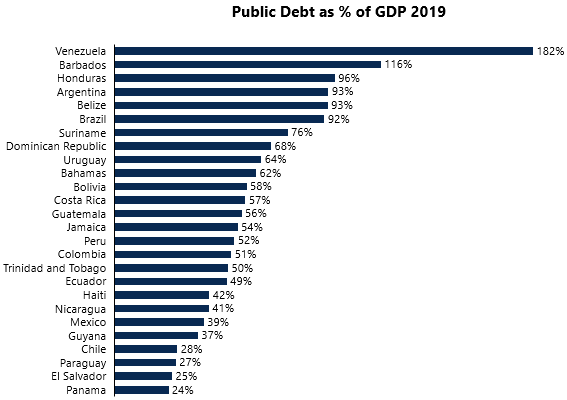

The LAC region presents a weak fiscal situation. No country in the region can afford the increases in spending carried out by developed countries to mitigate the impacts of the crisis. On average, public debt represented 62% of the GDP in 2019, compared to 40% of GDP in 2008. The high levels of debt will limit the response capacities of countries, and these will greatly vary as the levels of debt are very different between them.

In 2009, the region was able to respond to the international crisis with an average fiscal expansion of 3% of GDP. At the current debt levels, the response capacity today would be approximately 1.5% of GDP.

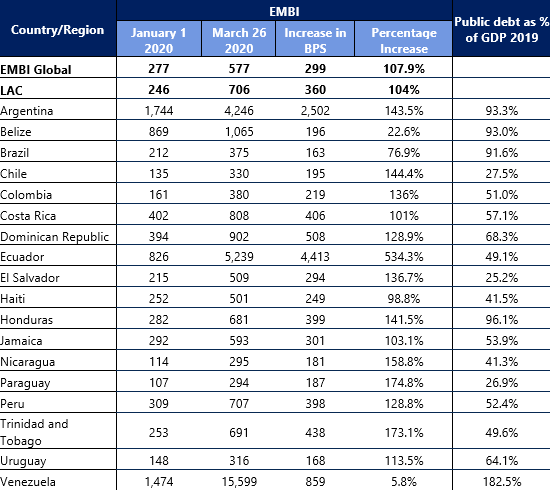

Moreover, the region’s capacity to access financing has also been affected by the crisis. According to data from the Emerging Markets Bond Index (EMBI), the cost of borrowing in for LAC countries doubled between January and March 2020. The region pays on average 700 basis points for external credit, but this varies between countries. Countries like Brazil and Chile can still access international credit at higher but “reasonable” rates, while for countries like Argentina and Costa Rica, the costs are so high that this is no longer a viable option.

Supporting Infrastructure: Internet, Healthcare & Social security

Digital technologies have enabled a transition to work-from-home and study/learning-from home, reducing the impact on some economic activities and education.

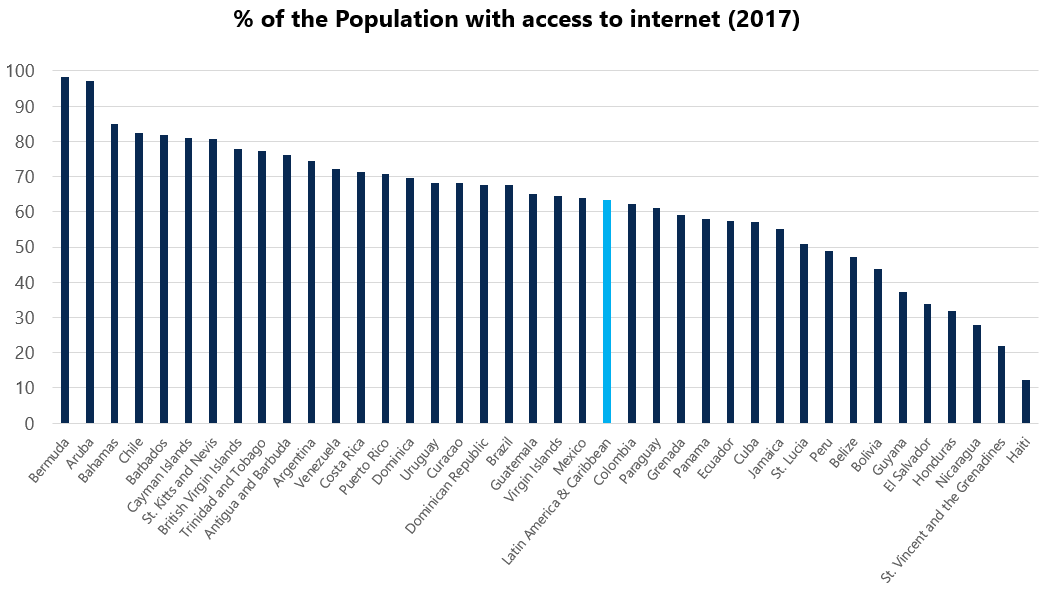

Although more than 67% of LAC’s population had access to internet in 2019, there are big differences in terms of access between countries. While +80% of the population has access to internet in countries like Bermuda, Aruba and Chile, this percentage drops below 50% in Peru and as low as 12% in Haiti. This is without considering the sub-national disparities between rural and urban populations, as well as income segments within each country, regarding access to internet.

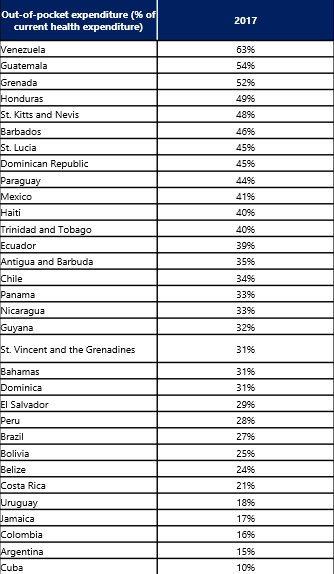

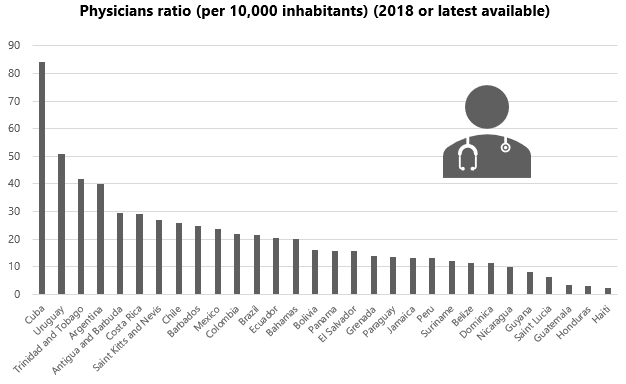

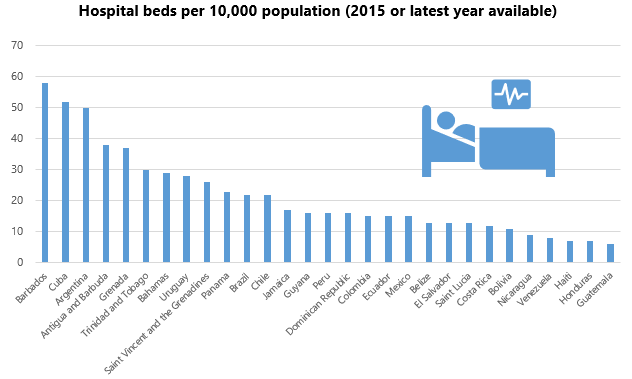

As for health services, the capacity of health systems in the region varies greatly between countries. The region’s government spending in health was 2.2% of GDP in 2018, far below the 6% of GDP recommended by the Pan American Health Organization (PAHO). In 2016, out-of-pocket health expenditure by households as a proportion of total current health expenditure in Latin America and the Caribbean (37.6%) was more than double that of the European Union (15.7%), and participation in health insurance plans for employed people aged 15 years and older was only 57.3%.

The LAC region has a serious deficit in hospital beds, including those in in- tensive care units (ICUs), and medical personnel (doctors, nurses, and others). In OECD countries, there are 3.5 doctors and 9.8 nurses per 1,000 inhabitants, whereas the comparable figures for LAC countries are 1.8 doctors and 4.4 nurses.

Source: UN-ECLAC Statistics

Moreover, health services in the region tend to be inadequate and not entirely accessible. In line with the low spending on healthcare, public services tend to be of varying quality, and private healthcare services are only available for those who can afford them. Furthermore, specialized healthcare services and physicians are mostly concentrated in key urban centers, making their access and affordability challenging for the low-income segments of the population.

Social protection systems in LAC will also face several issues, especially for countries with limited fiscal space. While these were already inadequate before the crisis, social protection systems will face several issues affecting their capacity to respond to the pandemic.

The region faces high rates of employment informality, with a regional average of more than 50% in 2017, limiting the access to social protection services and benefits. Only a few countries in the region have unemployment benefits. In 2019, only 6 countries (Argentina, Brazil, Chile, Colombia, Ecuador and Uruguay) had employment insurance for formal sector workers. Contributory social protection systems will face very high demands of sick leave benefits by workers, and the tax funded non-contributory social protection programs, which are normally designed to support the ported segments of the population, will need to be extended to cover low income families at risk of falling into poverty.

Policy recommendations

The pandemic has put countries in a situation on which they face 2 simultaneous crises: a health crisis, and an economic crisis. Given the limited fiscal space and costly access to finance for some countries in the LAC region., the response options are very limited. The link between the health and pandemic impacts will have governments juggle between different key objectives.

In the short term, the implementation of lockdowns, people movement restrictions and other social distancing measures are the most effective ways to fight the spread of the virus and control its mortality. However, general lockdowns also increase unemployment, declines in salaries, and increases poverty.

Governments do not have the fiscal resources to compensate the sectors affected by the pandemic. Therefore, governments must prioritize resource allocation. Naturally, allocating resources to one sector will reduce the resources available for another. The social context of the region will augment this tension. For instance, many households in the region were already poor before the pandemic, and any decrease in their income will put their survival at risk. On the other hand, households in the vulnerable middle class proportionally suffered the steepest decline on their incomes, so it will not be easy to balance the support given to both segments.

At the same time, governments must balance between supporting the sectors most affected by the pandemic (hotels, restaurants, etc.) and the workers of the many other sectors that will also be affected.

Typical support measures, such as cash transfers, will not be sustainable for extended periods of time, even in countries with greater fiscal resources. The current social support programs implemented by some countries in the region have limitations due to their design. These typically target segments classified withing structural poverty and are not designed to target vulnerable groups that are going through the transitory poverty caused by the pandemic.

While the specific measures will vary per country, according to their available resources, there are several recommendations that can be followed to tackle both crises.:

- A commensurate fiscal stimulus is needed to support health services and protect incomes and jobs. Countries must guarantee the supply of essential goods, such as medicines, medical equipment, food and energy, as well as universal access to testing and health care services.

- Health spending must be a priority, especially in countries with limited budgets. During the confinement period, resources must be focused on increasing the response capacity of the health system and expanding testing capacity.

- Mass targeted testing could be used to control infection rates among vulnerable populations. Focus mass testing efforts in targeted regions and hotpots on which the most vulnerable populations (i.e. those more pressed to go back to work, those most vulnerable or exposed to the virus) are concentrated. Serological tests would be the most efficient for this testing method on the LAC region, given that they are cheaper and do not require complicated technology.

- Social protection systems need to be strengthened to support vulnerable populations. Countries need to expand non-contributory programs, such as direct cash transfers, unemployment, underemployment, and self-employment benefits aimed at vulnerable population segments.

- Leverage and adjust already existing programs. Some countries in the region already had cash transfer programs in place before the crisis, which could be expanded and adjusted with new targeting instruments to cover poor and vulnerable population segments. Using alternative sources of data to identify vulnerable households, such as electricity consumption, application of employment benefits, or data from recent household censuses, can be used to identify priority targets.

- Housing crisis and massive business closures can be avoided by enabling mortgage and rent payment deferrals. Government should also consider deferring payments of basic services such as of water, electricity, and internet bills for low-income people for the duration of the pandemic.

- Central banks must ensure firms’ liquidity to ensure their operations can be carried out and the stability of the financial system. Central banks should intervene directly to provide the liquidity needed by the private sector.

- Prevent the collapse of the financial system by extending guarantees and credits to the banking sectors and other businesses whose closure would put financial stability at risk. While this measure will affect resources available for other interventions, it will benefit companies and economic sectors not benefited directly by other policies.

- Avoid the bankruptcy of businesses and minimize the decline in formal employment. Governments can extend loans and guarantees to businesses to provide liquidity. Temporarily suspend (moratorium) or reduce payments of taxes, mandatory contributions (except health insurance) and other regulations that increase the cost of production.

- Make the necessary legislative reforms to allow companies to temporarily reduce employment costs without permanent layoffs, such as temporary reduction of working hours and salaries. Immediate support should be provided to workers in MSMEs, low-income workers and those in the informal sector.

- International cooperation and multilateral organizations should design new technical and financial instruments to support countries facing fiscal pressures. They should also consider offering low-interest loans and debt relief and deferrals to open fiscal space.

- Multilateral institutions can go beyond financial support and provide technical assistance, by leveraging their areas of expertise and support networks, to help countries drat their response plans and their sequencing over time, and offer support in cross-cutting areas, such as big data and artificial intelligence to facilitate tracing, among other areas.

- Lift the sanctions on countries that are subject to them so they can have access to food, medical assistance and supplies, and COVID-19 tests.

- Ensure coordinated management of the response to the crisis. It is imperative that governments create high-level coordination mechanisms, especially given the multi-level government system in some countries, to establish and monitor goals and timeframes, allocate resources, and organize communication about the crisis.

- Ensure continuous and transparent communication with the general population, private sector, minorities, especially regarding the efficient and effective use of resources to fight the pandemic, to ensure public support and collaboration in the different measures.

Conclusions

While countries are already fighting the pandemic with using some and other policy measures, no response will be perfect. Governments will most likely have to implement and sustain multiple measures at a given time, by leveraging their available resources, and implement adjustments based on the results over time.

The crisis was certainly unpredictable, but as mentioned before, it has exhibited the many deficiencies in the economic and social systems developed by Latin American countries in previous decades. While countries must focus on fighting the pandemic today, once the crisis is over (hopefully soon), countries must look back to the past and rethink their development models to re-commence addressing the challenges that they have been dragging for decades, such as high levels of informality, poverty, untransparent fiscal management, access of basic services and build resilient and sustainable economies for the future.

Jesus Cazares – Senior Research Associate

Sources:

IADB

IADB

UN-ECLAC

UN-ECLAC

https://estadisticas.cepal.org/cepalstat/web_cepalstat/estadisticasIndicadores.asp?idioma=i

IMF June 2020 Economic Outlook: https://www.imf.org/en/Publications/WEO/Issues/2020/06/24/WEOUpdateJune2020

IMF October 2020 Economic Outlook:

https://www.imf.org/en/Publications/WEO/Issues/2020/09/30/world-economic-outlook-october-2020

World Bank

https://databank.worldbank.org/home.aspx