Scope 3 emissions

Scope 3 emissions

An increasing number of investors, consumers, and other stakeholders are demanding access to a comprehensive view of companies’ environmental impacts, along with climate-related risks. Companies that choose to report on their emissions usually only include information on their scope 1 and 2 inventories, thus excluding scope 3 emissions from their disclosures. However, given the mounting pressure from stakeholders and regulators, organizations may soon find themselves required to report on the full picture. Let’s take a look at a brief history of how the concept of emission scopes came to be and what they include, as well as regulatory trends related to scope 3 emissions.

The GHG Protocol and emission scopes

In the second half of the 1990s, both the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD) had come to the same conclusion: there was a clear need for an international standard for corporate greenhouse gas (GHG) accounting and reporting. WRI senior managers thus met with WBCSD officials in late 1997 and agreed to launch a new initiative, the GHG Protocol. With a core steering group combining members of environmental groups (e.g., WWF and the Pew Center on Global Climate Change) and industry (e.g., Norsk Hydro and Tokyo Electric), the multi-stakeholder standard development process took place. In 2001, the first edition of the Corporate Standard was published. It has since been updated with additional guidance.

The Corporate Accounting and Reporting Standard introduced the concept of “scopes” to help delineate direct and indirect emission sources.

- Scope 1 emissions refer to all direct GHG emissions, meaning emissions occurring from sources that are owned or controlled by the company.

- Scope 2 emissions refer to indirect GHG emissions from the consumption of purchased energy.

- Scope 3 emissions include all other indirect emissions.

Scope 3 emissions aim to capture all indirect emissions up and down a company’s value chain. While all scopes were introduced at the same time, the Corporate Accounting and Reporting Standard focused on the first two.

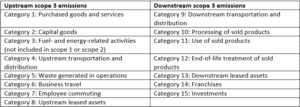

In order to help companies that wanted to account for GHG emissions across their entire value chain, the Corporate Value Chain (Scope 3) Accounting and Reporting Standard was published. The standard divides scope 3 emissions into 15 different categories:

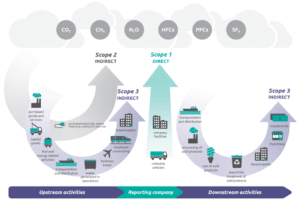

The figure below summarizes the concept of emission scopes by illustrating the entire value chain of an example company.

Companies are still lagging on emission disclosures

While companies are increasingly choosing to measure and disclose their scope 1 and 2 emissions, most are still very much lagging when it comes to scope 3. In its 2022 edition of the Global Supply Chain Report, CDP (formerly known as the Carbon Disclosure Project, one of the most popular voluntary reporting frameworks) revealed that while 72% of CDP-responding companies reported operational emissions (Scope 1 and/or 2), only 41% reported emissions for at least one Scope 3 category.

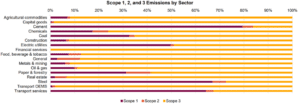

This is problematic, as scope 3 emissions usually account for the majority of a company’s total emissions. In a Technical Note published in 2022 (revised in 2023), CDP provides an analysis that highlights the crucial importance of scope 3 reporting: across all sectors, Scope 3 emissions account on average for 75% of total Scope 1+2+3 emissions in the sample. The organization also provides the breakdown by sector, as shown in the figure below.

Regulatory pressure

The regulatory landscape is shifting towards more comprehensive disclosures. The International Sustainability Standards Board (ISSB), announced during COP26 in Glasgow, is one of the standard-setting boards of the IFRS Foundation. The ISSB’s standards provide a comprehensive global baseline for sustainability disclosure. In March 2022, it launched a consultation on two proposed standards for general sustainability-related disclosure requirements (IFRS S1) and climate-related disclosure requirements (IFRS S2). In October 2022, the ISSB unanimously voted to require company disclosures on the three GHG emission scopes, applying the current version of the GHG Protocol Corporate Standard as part of IFRS S2. In June 2023, the ISSB finalized and issued the standards. While not mandatory on their own, the ISSB is backed by groups such as the G7 and G20, and it works with jurisdictions on the regulatory adoption of these standards as well as to facilitate compatibility and interoperability. For example, the UK government announced in August 2022 that the ISSB standards would form a core part of the Sustainability Disclosure Requirements (SDR) regime it is working on developing. In July 2023, the International Organization of Securities Commissions (IOSCO) announced its endorsement of IFRS S1 and IFRS S2, calling on its 130 member jurisdictions (which regulate more than 95% of the world’s financial markets) to consider ways in which they might incorporate these standards into their jurisdictional arrangements.

In the European Union, Directive (EU) 2022/2464, also known as the Corporate Sustainability Reporting Directive (CSRD), entered into force in January 2023. The CSRD aims to ensure that stakeholders have access to the needed information to assess the impact of companies on environmental, social, and governance matters and that investors are able to assess financial risks and opportunities related to climate change and other sustainability issues. It also broadens the set of companies that will now be required to report on sustainability, relative to previous regulations. The CSRD requires Scope 3 reporting (although smaller companies are exempt from this), and the first companies will have to apply the new rules for the first time in the 2024 financial year for reports published in 2025.

In the United States, the Securities and Exchange Commission (SEC) unveiled in March 2022 a proposal that would require publicly listed companies to disclose their GHG emissions and any climate-related risks to their operations. Scope 3 reporting would be required if deemed material or if the company has set an emission target or goal that includes scope 3 emissions. The SEC was initially expected to issue its final climate risk disclosure rule in December 2022, but it pushed it back to the end of April 2023. In the same month, a former SEC commissioner revealed the rule would be delayed until the fall. Current efforts in the country also include bills introduced by the states of California and New York, which propose to further strengthen companies’ obligations to disclose their GHG emissions, including scope 3 categories.

These are only a few examples, and given the global, interconnected nature of supply chains today, it is becoming increasingly urgent for companies that do not already report on their GHG emissions to prepare for the upcoming changes and take the necessary steps to ensure compliance. Organizations need to identify regulations relevant to their operations and familiarize themselves with the expected requirements.

Finally, while one of the most frequent complaints relates to the complexity of scope 3 measurements and control, guidance from trusted organizations is available. We already mentioned above the Corporate Value Chain (Scope 3) Accounting and Reporting Standard, published by the GHG Protocol, along with a Technical Guidance for Calculating Scope 3 Emissions. Other helpful documents include, for example, the “Value Change in the Value Chain” guidance report, published by the Science Based Targets initiative (SBTi), Navigant and the Gold Standard, which provides best practices in scope 3 GHG management. SBTi also offers other helpful resources, such as sector-specific guidance for a growing list of industries.

Sources:

https://ghgprotocol.org/about-us

https://ghgprotocol.org/sites/default/files/standards/ghg-protocol-revised.pdf

https://ghgprotocol.org/calculation-tools-faq

https://ghgprotocol.org/sites/default/files/standards/Scope3_Calculation_Guidance_0.pdf

https://www.ifrs.org/news-and-events/news/2023/06/issb-issues-ifrs-s1-ifrs-s2/

https://www.iosco.org/news/pdf/IOSCONEWS703.pdf

https://www.sec.gov/news/press-release/2022-46

https://www.complianceandrisks.com/blog/esg-reporting-developments-in-the-united-states/

https://www.persefoni.com/learn/scope-3-reporting-challenges

https://sciencebasedtargets.org/resources/files/SBT_Value_Chain_Report-1.pdf