Debt Distress and The Sustainable Development Agenda: Unfulfilled Goals?

Table of Contents

The global debt pile is mounting at an alarming pace, with a stock of $305 trillion in 2023, recording a staggering surge of $100 trillion over the past decade, as the Institute of International Finance highlighted. The World Bank identifies the emerging risk of entering ‘a fifth wave’ of a debt crisis. This implies a threat to low-income countries, endangering their ability to fulfill the pledge of “Leaving no one Behind” in the journey towards sustainable development.

The United Nations shaped this ambitious promise in 2015, aiming to fulfill it by 2030 and eradicate poverty and curb all forms of inequality. It is already halfway to 2030, and with the cascading crises that the world witnessed, from the outbreak of COVID-19 and the war in Ukraine to climate disasters worldwide, the financing needs of developing countries to counter the shocks are rising, as is their cost of debt service.

“Countries are facing the impossible choice of servicing their debt or serving their people”.

The United Nations Secretary,General António Guterres,July 2023

The Debt Trap: Soaring Poverty and Hunger

Public debt is deemed “sustainable” when the government can fulfill its present and future payment commitments without requiring exceptional financial aid or facing the risk of default. The primary instrument creditors use to evaluate the risk of default in Lower-Income Countries (LICs) is the Debt Sustainability Framework (DSF) developed by the World Bank. This framework categorizes countries according to their capacity to repay their debt obligations, establishes threshold levels for specific debt burden indicators, and stress-tests scenarios in comparison to these thresholds. According to this framework, over 40% of low-income countries are already approaching debt distress (unsustainable) levels.

There is a vicious circle between debt and achieving the Sustainable Development Goals (SDGs), where mounting debt puts a heavy strain on mobilizing public resources dedicated to investments in the economy and people’s well-being.

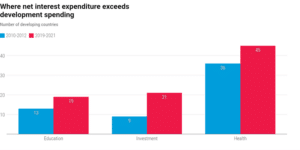

In fact, around 3.3 billion people live today in countries that spend more on interest payments than on education, health, climate adaptation, and social protection, according to the United Nations.

Source: UNCTAD 2022

Source: UNCTAD 2022

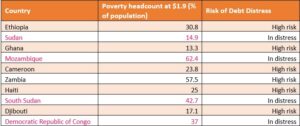

Meanwhile, global hunger (Sustainable Development Goals 2) is soaring amid the dire economic effects of political conflicts and climate change, whereby the number of undernourished people has grown by as many as 150 million in the last 10 years. Ethiopia, for instance, where 4% of the global population is extremely poor, was already at high risk for debt distress, even before the pandemic crisis.

Source: Sustainable Development Goals in the Debt Trap, June 2022, extracted from the World Bank Debt Sustainability Analysis, https://www.worldbank.org/en/programs/debt-toolkit/dsa.

Unprecedented Record: Don’t solely blame the pandemic.

Even before the cascading crises, the pandemic and the Russian War posed a major threat to advancing the Sustainable Development Goals. Moreover, the cost of debt servicing for countries eligible for international development assistance more than doubled between 2000 and 2019. (UNDESA, 2020). In 2022, 69 low- and middle-income countries made payments of $62bn on public debt, which means a 35% increase from 2021. On this front, the UN issued an alarming warning as global public debt reached a record of $92 trillion in 2022. According to the IMF, public debt as a ratio to GDP has soared across the world during COVID-19; the global average of this ratio in 2020 approached 100 percent, and it is expected to remain above pre-pandemic levels for about half of the world.

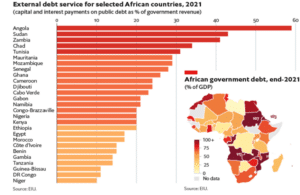

Source: EIU

Debt and Climate Change: Bidirectional Causality

The vicious circle of debt is even more intertwined with the threat of climate change (Sustainable development goal 13), whereby countries that are most vulnerable to the climate crisis are also the ones on the frontlines of sovereign default. In fact, UNCTAD outlines that over 70% of current public climate finance takes the form of debt. Meanwhile, the UN Environment Programme estimates that the annual climate adaptation needed for developing countries could amount to $340 billion by 2030 and $565 billion by 2050. Today, around 60% of the poorest countries are already in debt distress or on the brink of it; among these are Sri Lanka, Ghana, Lebanon, and Zambia.

The causality between debt distress and climate change is bidirectional. In developing nations, constrained governmental budgets pose a challenge: they hinder the ability to make investments needed for a climate-resilient recovery. Simultaneously, studies provide empirical evidence that the exposure of sovereigns to climate risks can impact credit ratings and debt servicing costs. Addressing this issue, the IMF empirically demonstrates that countries with higher resiliency to climate change shocks enjoy elevated credit ratings. The IMF also argues that the impact of climate change is disproportionately greater in developing countries, due largely to a weaker capacity to mitigate the consequences of climate change. African countries, the Middle East, and Latin America are the regions least resilient to climate change shocks.

A possible way out

Amid substantial financing requirements spanning over a wide range of countries, reminiscent of the levels witnessed during the 1980s debt crisis, a rising demand for debt restructuring is emerging.

Structural fiscal reform

The World Bank suggests long-term remedies such as ramping up economic growth, whereby the best way to escape a debt trap is “to grow out of it”. Growing out of debt can be done through improving business conditions, better allocation of resources, and healthy market competition to boost productivity.

On the structural reform front, the WB stresses the importance of accelerating fiscal policy reforms through improving tax administration efficiency and broadening the tax bases in ways that support rather than impede long-term growth. That can be accomplished by improving tax compliance, debt management procedures, and public spending while strengthening the legal environment for debt contracting.

DEBT RESTRUCTURING

While fiscal consolidation and growth-oriented structural reforms have the potential to diminish debt ratios, they might not suffice for nations grappling with severe debt issues or the heightened risks associated with debt rollovers. In such instances, it may become imperative to undertake debt restructuring, which involves renegotiating the terms of a loan.

For vulnerable middle-income countries, the United Nations proposes several urgent solutions to alleviate the ballooning debt; these encompass payment suspensions, longer lending terms, and lower interest rates. The G20 had several contributions on this front; they assisted low-income nations through the suspension of loan and interest repayments until mid-2021, known as the Debt Service Suspension Initiative (DSSI), and then through the Debt Service Suspension Initiative (DSSI).

Typically, debt restructuring is employed as a measure of last resort due to its potential for considerable economic costs, reputational risks, and challenges in terms of coordination. Despite these challenges, when coupled with fiscal consolidation, debt restructuring can significantly decrease debt ratios by up to 8% or more over a five-year period, as noted by the IMF

Debt Swaps

Unlike debt relief, debt swaps come with conditions for external debt alleviation, necessitating the allocation of domestic funds to activities tied to the Sustainable Development Goals. These activities encompass health, education, child development, and environmental preservation. Debt swaps can take the form of equity investments (equity swaps), environmental activities (environmental swaps), or development activities (development swaps).

Egypt is a salient example of a development debt swap; in 2001, the country signed an agreement with Germany to swap 50% of its debt amounting to 204.5 million euros to finance projects in the areas of poverty reduction, improving water and sanitation infrastructure, improving basic education, and environmental protection. A more recent example of development debt swaps is in 2017, when the Global Fund to fight Aids, Tuberculosis, and Malaria (GFATM) declared that Spain had signed agreements to withdraw 36 million euros of debt to the Democratic Republic of Congo, Cameroon, and Ethiopia. In return, the countries would invest a total of 15.5 million euros in health-related projects.

Conclusion

Amid ballooning inflation, the surge of interest rates, and sluggish growth, governments in developing countries are now burdened with alarming levels of public debt, forcing them to choose between paying debt service or investing in their nations. To mitigate the trade-off between “investments in debt and investments in people”, focusing on the reforms of global debt architecture (debt relief, restructuring, swaps, etc.) as well as finding innovative financing schemes is of utmost importance to prevent exacerbating poverty and “a lost decade of inaction”.

Sources

https://www.barrons.com/news/world-facing-5th-wave-of-debt-crisis-world-bank-chief-01665154807

https://unsdg.un.org/2030-agenda/universal-values/leave-no-one-behind

https://www.actionagainsthunger.org/the-hunger-crisis/world-hunger-facts/

https://www.imf.org/en/Publications/WEO/Issues/2023/04/11/world-economic-outlook-april-2023

https://unctad.org/news/un-warns-soaring-global-public-debt-record-92-trillion-2022

https://www.imf.org/en/Publications/WEO/Issues/2023/04/11/world-economic-outlook-april-2023

https://link.springer.com/article/10.1007/s10584-022-03373-4

https://blogs.worldbank.org/voices/when-debt-crises-hit-dont-simply-blame-pandemic