Winds of Change in Sub Saharan Africa

Table of Contents

Winds of change have been blowing impetuously in some Sub-Saharan African (SSA) countries in the last months. Although change is always quite welcome when it comes during a gloomy period, it often goes hand-in-hand with a degree of uncertainty that requires action to be measured and possibly mitigated.

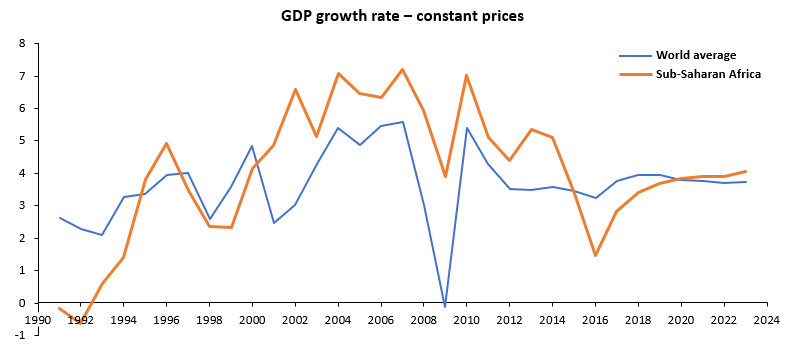

The low period of discussion started in 2015, when Sub-Saharan Africa growth began to dip below the world average for the first time since 2000. It reached its gloomiest point in 2016, with a GDP growth rate of +1.4% — the lowest in 22 years.

For 2018, the IMF forecasts an encouraging +3.4% growth rate, but the Fund also says that to effectively catch up the rest of the world, the SSA will have to wait until 2020.

Normally, mid-sized economies can ensure (or at least protect) growth as long as enlightened investments in infrastructure, innovation and expansion of the internal consumption can be guaranteed.

In other cases, the sole recent recovery of commodity prices seems like such a fragile driver for the future, as it has been in the past. Structural reforms to the economy and governance have been long awaited, but a decisive shock may have finally have occurred.

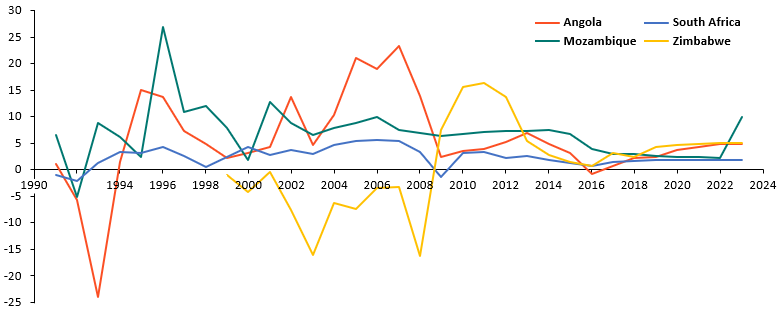

Winds of Change in Angola

Last September Angola elected its new president after 38 years under Jose Eduardo Dos Santos. But the real end of the dynasty seemed to be the decision of Joao Lourenço, Angola’s new president, by removing Eduardo’s daughter and son from the guidance of two pillars in the local economy. Respectively this included, Sonangol, the national oil company, and a 5 billion USD sovereign wealth fund.

Lourenço has seemed very determined to fight corruption, make Angola more attractive to foreign investors (i.e. by removing obligations of Angolan business ownership) and dismantle some previously existing mechanisms that kept two-thirds of Angolans under the poverty line despite the oil boom.

Winds of Change in Zimbabwe

The newly elected President of Zimbabwe, Emmerson Mnangagwa, recently asked its people for their patience. After 37 years of dictatorship under Robert Mugabe, the current president is trying to take appropriate actions to bring the country back on track.

Internally, he’s actively combating corruption by arresting several high-profile individuals on allegations of bribery. Additionally, he’s implementing social welfare measures such as providing free medical care for children and people over the age of 70, as well as enacting a temporary reduction in fuel prices. Externally, he has reached agreements with South Africa to upgrade the shared railway network and with China to expand Harare airport’s capacity. He is also actively looking for partnerships and investors to revive the Zimbabwean economy through further deals with Belarus, Russia and, again, China.

Winds of Change in South Africa

Elected last February, the new president, Cyril Ramaphosa, has promised to secure a total of USD 100 billion US dollars of investment for the country and, more importantly, stop the opaque misconduct of state-run firms and make clean governance a priority.

Taking over the inheritance of 9 years under Jacob Zuma, whom recently appeared in court to face 16 corruption charges, means finding a delicate balance between the required rupture with the past and the current need for governability. Corruption has undermined public confidence within state institutions and, given South Africa’s economic significance within SSA, Ramaphosa has not only South African eyes on him.

Mozambique

The unpredictable death (by natural causes) of Afonso Dhlakama, leader of the historical opposition party for over 40 years, casts shadows on the continuation of the peace treaties with the ruling party. This conflict has dragged on since when Mozambique became independent and, in the opinion of many, has been a brake on the social and economic development of the country.

With presidential elections scheduled for next October, the attitude toward peace and democracy of those who will succeed Dhlakama has kept everyone on hold. Truth is that Renamo, the recently orphaned party, gained momentum in the 2014 general election and kept it in recent by-election in the Nampula province. Moreover, in five months the electorate could finally express its opinion on the scandal over the giant debt incurred during the 2013 Guebuza administration and unveiled only in the last parliamentary term.

Apart from legitimate skepticism and subjective political orientations, these vicissitudes will surely have an impact both on regional and individual country scenarios. Ultimately, companies and investors will be called to analyze and re-assess their business operations, based on where the wind blows.

Antonio Pilogallo, Senior Associate at Infomineo

Sources

- https://www.reuters.com/article/us-china-zimbabwe/chinas-xi-tells-zimbabwe-president-they-should-write-new-chapter-in-ties-idUSKCN1HA1LF

- https://www.economist.com/news/middle-east-and-africa/21742130-just-he-was-about-agree-peace-deal-warlord-drops-dead-will-afonso

- https://www.economist.com/news/middle-east-and-africa/21741577-how-far-will-he-go-fighting-corruption-angolas-new-president-jo-o

- https://www.economist.com/news/middle-east-and-africa/21742135-risks-remain-africas-economies-are-turning-corner

- https://www.economist.com/news/middle-east-and-africa/21742135-risks-remain-africas-economies-are-turning-corner

- https://www.nytimes.com/2018/02/26/world/africa/south-africa-ramaphosa-cabinet.html

- https://www.theguardian.com/world/2018/feb/14/who-is-cyril-ramaphosa-south-africa-president

- http://allafrica.com/stories/201805150081.html

- World Economic Outlook Database, April 2018